The Definitive Guide to Paying Taxes as a Real Estate Agent

Here’s the information you’ll need to make tax time go as smoothly as possible.

Learn more about life as a real estate agent and get exclusive offers!

Income tax returns are a complicated business. And they’re even more complex for real estate agents because agents are typically self-employed, which comes with a different set of tax rules than being a traditional employee.

Whether you plan to calculate and file your income taxes on your own or hire an accountant to do your taxes, here’s the information you’ll need to make tax time go as smoothly as possible.

This is your definitive guide to paying taxes as a real estate agent.

Income Tax Basics

Let’s start with the basics. In this section, we’ll cover the fundamentals of income taxes, specifically as they apply to real estate agents.

Understanding the Difference Between Employees and the Self-Employed

The vast majority of real estate agents are not employees. They are “independent contractors” (self-employed for all intents and purposes). And this distinction comes with a few key differences in how income taxes are paid.

Withholdings

Employees have money withheld from their paychecks, by their employers, to pay their income taxes. The money is taken from their earned wages and whisked off to the government before the employee even sees it.

The self-employed, on the other hand, are completely responsible for paying their own taxes. So unless you are legally considered an employee in your real estate brokerage (which is exceedingly rare), your broker will not withhold money from your commission checks for your taxes.

Instead, you need to send periodic tax payments to the IRS on your own. These payments are just estimates of taxes due. You’ll still reconcile your taxes for the year with an annual filing, due on April 15th.

You can send your periodic payments as often as you like (after every closing, for example). But you must make payments at least quarterly if you expect to pay more than $1,000 in taxes for the year.

The quarterly due dates typically follow the same schedule every year (but you should still confirm the dates each year just to be sure):

January 15: taxes due on income earned between September 1 and December 31 of the previous year

April 15: taxes due on income earned between January 1 and March 31

June 15: taxes due on income earned between April 1 and May 31

September 15: taxes due on income earned between June 1 and August 31

You are responsible for making sure your tax payments have been submitted (at least postmarked if you’re mailing them in) by these quarterly due dates.

Self-Employment Taxes

Employees also have social security and Medicare taxes withheld from their paychecks.

But as self-employed, real estate agents are required to pay Self-Employment Taxes to cover their share of Social Security and Medicare. These self-employment taxes are paid just like your income taxes: you can pay them as often as you like, but you must pay at least quarterly according to the schedule above.

Getting Ready To Renew Your License?

Take our online continuing education courses and renew your real estate license today!

Understanding Tax Brackets

The percentage you pay in income tax depends on your taxable income for the year, as well as your filing status (Single, Married - filing jointly, Married - filing separately, Head of Household).

Here are the tax bracket percentages for income earned in 2024 (directly from the IRS):

It’s important to note that these amounts are based on taxable income. Your taxable income will be less than your actual income because you’ll be able to take deductions (mostly to offset your costs of doing business — we’ll get into all that in just a bit!).

You can see how it’s difficult to know how much to pay in periodic tax payments when you can’t be sure how much income you’ll make for the year or how much you’ll be able to deduct from your income to arrive at your taxable income.

This is why your periodic tax payments are just estimates. You can make an educated guess at your annual income and deductions, and pay your taxes accordingly. IRS Form 1040-ESAbout Form 1040 Es Forms PubsAbout Form 1040 Es Forms Pubs (which is the form you’ll use to file your periodic payments) will also help you with these calculations.

And don’t forget to pay your self-employment taxes on top of your income taxes. The current self-employment tax rateSmall Businesses Self Employed Self Employment Tax Social Security And Medicare Taxes Businesses is 15.3% (12.4% for Social Security + 2.9% for Medicare) for net income up to $168,600 for the year. For any net income over $168,600, you’ll pay the same 2.9% for Medicare, but you won’t have to pay the 12.4% for Social Security.

As a general rule of thumb, it’s wise to set aside 30% of your income to cover your income taxes plus the self-employment tax.

Understanding the Forms

The tax return forms are different for independent contractors than for employees. Here’s a quick look at the different forms you’ll use as a self-employed worker.

1099-MISC

1099-MISCAbout Form 1099 Misc Forms Pubs is the document that reports your income. Your broker will give you a 1099-MISC form every year to show how much money you made working as an independent contractor for that broker throughout the year. (You may be familiar with employee W-2s; the 1099-MISC is the equivalent of a W-2, but for the self-employed.)

Form 1040-ES

Form 1040-ESAbout Form 1040 Es Forms PubsAbout Form 1040 Es Forms Pubs is more of a booklet than a form. This is the document you’ll use to estimate and pay your quarterly taxes.

Form 1040

Form 1040About Form 1040 Forms Pubs is your annual tax return form. This form is standard for everyone reporting individual income tax, but as a self-employed worker, you get to fill out a few additional schedules on Form 1040:

Schedule SE: used to calculate your self-employment taxes

Schedule C: used to calculate your net profit from your real estate business

Understanding State Income Taxes

Generally speaking, Americans pay two levels of income taxes: Federal and State. This post is focused on federal income taxes since those apply to all real estate agents nationwide. But you should know that you may also be required to pay additional state taxes (on top of the federal taxes covered in this post).

Rather than try to provide details on all 50 states, we will simply let you know which states levy a state income tax, and which states don’t.

States with NO State Income Tax

If you live in one of the following states, congratulations! You don’t have to pay any state income tax:

Alaska

Florida

Nevada

South Dakota

Tennessee

Texas

Washington

Wyoming

States with Limited State Income Tax

New Hampshire residents don’t have to pay any state income tax on income made in their line of work, but they do pay state income tax on income earned from investments.

States that Levy Full State Income Taxes

If you aren’t in one of the nine states mentioned so far in this section...sorry. You have to file and pay state income taxes on top of your federal income taxes.

Understanding Tax Deductions vs. Tax Credits

Now we’re getting into the nitty-gritty of income tax. Tax deductions and tax credits both save you money on your income taxes, but they are different.

Tax Deductions

Commonly called tax write-offs, deductions are amounts subtracted from your total income, so you’re essentially taxed on a lower amount than you actually earned.

Taxpayers have two options for deductions:

Take the standard deduction. For 2024, standard deductions are as follows: Single or Married - Filing Separately can deduct $14,600, Married - Filing Jointly or Qualifying Surviving Spouse can deduct $29,200, and Head of Household can deduct $21,900.

Itemize your deductions. If your deductible expenses exceed the standard deduction, you can itemize them, which means to list and claim them individually.

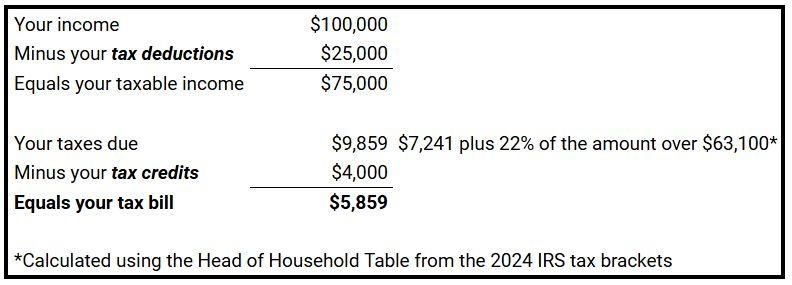

Example: You earned $100,000 in income and spent $25,000 on deductible business expenses. Since your deductions exceed the standard deduction, you’re better off itemizing. This allows you to subtract the $25,000 in expenses from the $100,000 income. So you’ll be taxed on just $75,000, rather than the full $100,000).

Tax Credits

Tax credits are amounts subtracted directly from your calculated taxes due.

Example: After subtracting your deductions, your taxable income is $75,000. If you’re filing as the head of household, your taxes would be $9,859 ($7,241 plus 22% of the amount over $63,100 according to the tax bracket table). Now, if you have two kids, you can take a $4,000 child tax creditIndividuals Refundable Tax Credits Credits Deductions which would be subtracted from the calculated taxes. So your tax bill would be reduced to $5,859.

Example of Tax Deductions and Credits at Work Together

It may help to see an example of deductions and credits working together:

Now that we know the difference between tax deductions and tax credits, let’s look at some of the common deductions and credits used by real estate agents.

Tax Deductions for Real Estate Agents

As an independent contractor, you’ll have a lot of business expenses to write off. Your tax filing software or tax accountant will walk you through all the specific requirements for claiming these write-offs. You can also find information for all deductions available to businesses on the IRS websiteBusinesses Credits Deductions.

The key to getting your deductions right is to make sure your business expenses are “ordinary and necessary” — the expression used by the IRS to determine if business expenses are legitimate. Yes, it’s vague, but use your best judgment. Can you write off a private plane as a real estate business expense? Maybe if you sell luxury real estate in Hawaii and need to fly your clients between islands. Otherwise, no.

Here is a list of the more common real estate agent deductions:

The Home Office Deduction or Office Rent: If your primary place of business is your home office, and that area of your home is used exclusively for work, you can deduct the cost of maintaining your home office. You can choose between the standard deduction of $5 per square foot (up to 300 SF), the cost of your mortgage and utilities allocated to that square footage, OR the cost of furniture, renovation, and decoration. If you rent an office instead of working from home, your rent cost (or desk fee) is deductible.

The Vehicle Deduction: You can deduct the cost of using your vehicle for business. You can either track your work-related mileage to use the standard mileage rate ($0.67 per mile in 2024), OR you can track the actual cost of gas and maintenance and insurance and multiply that total by the percentage of the time the vehicle is used for business (as opposed to personal use).

Retirement Plan Contributions: You can contribute the legal maximum to your retirement account (like an IRA), and deduct the full amount on your tax return.

Internet and Phone Service: Deduct the portion of your internet and phone service used for business.

All Office Supplies and Equipment (Including Technology): All office supplies are deductible. Think desk chair, paper, pens, your work computer, your work phone, real estate softwareReal Estate Agents Ultimate Guide Proptech Blog, a printer...all deductible.

All Marketing: Everything you do to market your businessReal Estate Marketing 101 Blog is deductible. Your website, Facebook ads, client gifts, signage, mailers, billboards, etc.

All Professional Services: Legal and accounting (including tax prep!) fees are deductible, as are fees paid to your assistant (even if the assistant is virtual), your blog writer, and your website designer. E&O insurance is also deductible, as is real estate coaching, continuing educationReal Estate Continuing Education, industry conferences, membership dues, and subscriptions to industry publications.

Tax Credits for Real Estate Agents

Every tax credit comes with its own rules. And many credits are phased out if your income is over a certain dollar amount. For example, the Daycare Credit starts at 35% of the expense for families who make less than $15,000 but shrinks by one percentage point for every $2,000 more you make in income.

As with deductions, your tax filing software or tax accountant will walk you through all these specific rules to see how much of a credit you qualify for. You can also find information about all the tax credits we’ll discuss (plus all the additional tax credits available) in the Tax Credits Section of the IRS websiteTax Credits For Individuals What They Mean And How They Can Help Refunds Newsroom.

Here are the common tax credits you may qualify for as a real estate agent:

Education credits: If you or your dependent children are taking courses in higher education, you may be able to receive a tax credit. The American Opportunity Credit is for undergrad students (with no felony convictions) enrolled at least half-time. It can be up to $2,500 per year.

The Saver’s Credit: If you contribute to a retirement account (like an IRA), you might qualify for a credit of between 10% and 50% for up to $2,000 in contributions.

The Residential Energy Credit: Did you make your home more energy efficient by adding solar panels or a solar water heater? You can get a credit for up to 30% of the cost!

The Child Tax Credit: If you have kids, you could qualify for up to $2,000 per child.

Child and Dependent Care: When you pay for childcare (or adult care for incapacitated adults), you can receive a credit of 20-35% of up to $3,000 in care costs.

The Earned Income Credit: If you make less than the threshold based on your filing situation, you may qualify for the earned income credit. This is a general credit available to all Americans with qualifying income.

The 7 Biggest Tax Mistakes Real Estate Agents Make

To help you avoid some of the pitfalls of filing taxes as a real estate agent, let’s count down the top seven biggest mistakes real estate agents make on their taxes.

Mistake #7. Losing Track of the Recent Tax Code Changes

Sections of the U.S. Tax Code are always changing. And many agents (many Americans in general, actually) struggle to keep track of the changes. But it’s important to note changes that will have a substantial impact on your income taxes.

For example, from 2020 through 2022, businesses could deduct 100% of business meals. However, the deduction reverted to 50% starting in 2023.

Mistake #6. Ignoring the Home Office Deduction

Back in the day, real estate agents were hesitant to take the home office deduction because it was seen as a “red flag” that could trigger an IRS audit. But that’s no longer the case.

With so many Americans currently working from home (as employees or self-employed), it’s quite common for people to claim home office deductions. And the IRS no longer flags them as suspicious.

You just need to make sure your home office is used exclusively for work (it can’t be a shared family space, like a dining room for example), and that it is your principal place of business. If you work more from your broker’s office, you probably can’t claim the home office deduction. But if you work mostly from home, maintaining that designated square footage as an office is a legitimate business expense.

Mistake #5. Mixing Personal and Professional Finances

Tax filings can get messy. Especially when you have as many out-of-pocket business expenses as real estate agents do!

To keep your records clean and easy to follow, keep your professional finances separate from your personal finances. Open a separate checking account, and get a separate credit card that you use exclusively for your business transactions. When you get your commission check, deposit it into your business account, and then “pay yourself” by transferring some of that money to your personal account.

Whether you’re filing your own taxes or you’re hiring a professional, having a separate account for personal and professional records will make the filing process cleaner and simpler.

Mistake #4. Overlooking Deductions and Credits

With all the deductions and credits available to real estate agents, it’s easy to overlook some of them.

Keeping careful records of all your business expenses throughout the year will help you recall some of those expenses and remember to deduct them. Which brings us to Mistake #3.

Mistake #3. Failing to Track Income and Expenses

You can’t possibly capture all your deductions if you’re not tracking your business expenses.

Don’t forget to keep your receipts and invoices as a backup (you can always snap a quick photo on your phone and just save the images to your computer). The IRS doesn’t consider credit card statements as proof of expenses because they don’t itemize the expenses. In case of an audit, the burden of proof lies with the taxpayer; you have to prove that your deductions are legitimate. So make sure you have a complete backup to support every deduction.

Tracking your income is just as important. If you offer services to your clientsOffer These 5 Real Estate Services And Watch Business Skyrocket separate from your commission-based real estate transactions, you need to record all that extra income.

Mistake #2. Missing Filing or Payment Due Dates

While employees only need to worry about April 15th, self-employed individuals like real estate agents need to remember all four quarterly due dates. Missing a due date, or underpaying your estimated taxes by more than 10%, will result in penalties plus interest.

Generally, the penalty is around 5% of the underpayment of taxes. But it gets a little more complicated than that. If you think you may have accidentally underpaid or missed a quarterly estimated payment, IRS Form 2210I2210 Instructions can help you calculate your penalty due.

Set yourself event reminders for future quarterly dates. And set those reminders to warn you well in advance of the due date so you have time to calculate your estimated tax payments and send in your payment before it’s due.

Mistake #1. Not Hiring a Tax Professional

Obviously, there is quite a lot to this whole real estate agent income tax thing! You don’t know all the ins and outs like a tax professional does.

As a real estate agent, you often have to convince sellers that they’re better off paying you to sell their home than trying to go FSBO to save money. It’s the same with tax professionals.

You might save on the tax preparation fees by doing your own taxes, but you could end up paying much more in taxes than you need to. You’re usually better off spending the money to hire a tax professional to ensure that you don’t overpay in taxes or end up with a silly penalty for an accidental oversight.

Helpful Income Tax Resources for Real Estate Agents

Here are a few useful resources to help real estate agents navigate the world of income tax.

The IRS

You can always get information directly from the source! The IRS has a tax tip guide specifically for real estate agentsSmall Businesses Self Employed Licensed Real Estate Agents Real Estate Tax Tips Businesses.

Accounting Software

Consider investing in accounting software to help you stay on top of your income and expenses. Here are a few options to check out:

Quickbooks

Freshbooks

Realtyzam

Xero

Tax Prep Services

Spend some time reviewing Certified Public Accountants (CPAs) in your local area to find a tax preparer you like and trust. Don’t simply go to a tax prep company like H&R Block and allow just anyone to tackle your tax return. Make sure you get a CPA, preferably with experience handling real estate agent filings.

But that’s not your only option for filing your taxes. You can also try tax software like TurboTax Self Employed, H&R Block Premium, or TaxAct if you want to attempt your own tax filing.

Whether you decide to go it alone or hire a pro, we hope you’ve found this definitive guide to paying taxes as a real estate agent useful!

Looking for more real estate career news and CE course discounts? Subscribe to Aceable today and stay in the loop!